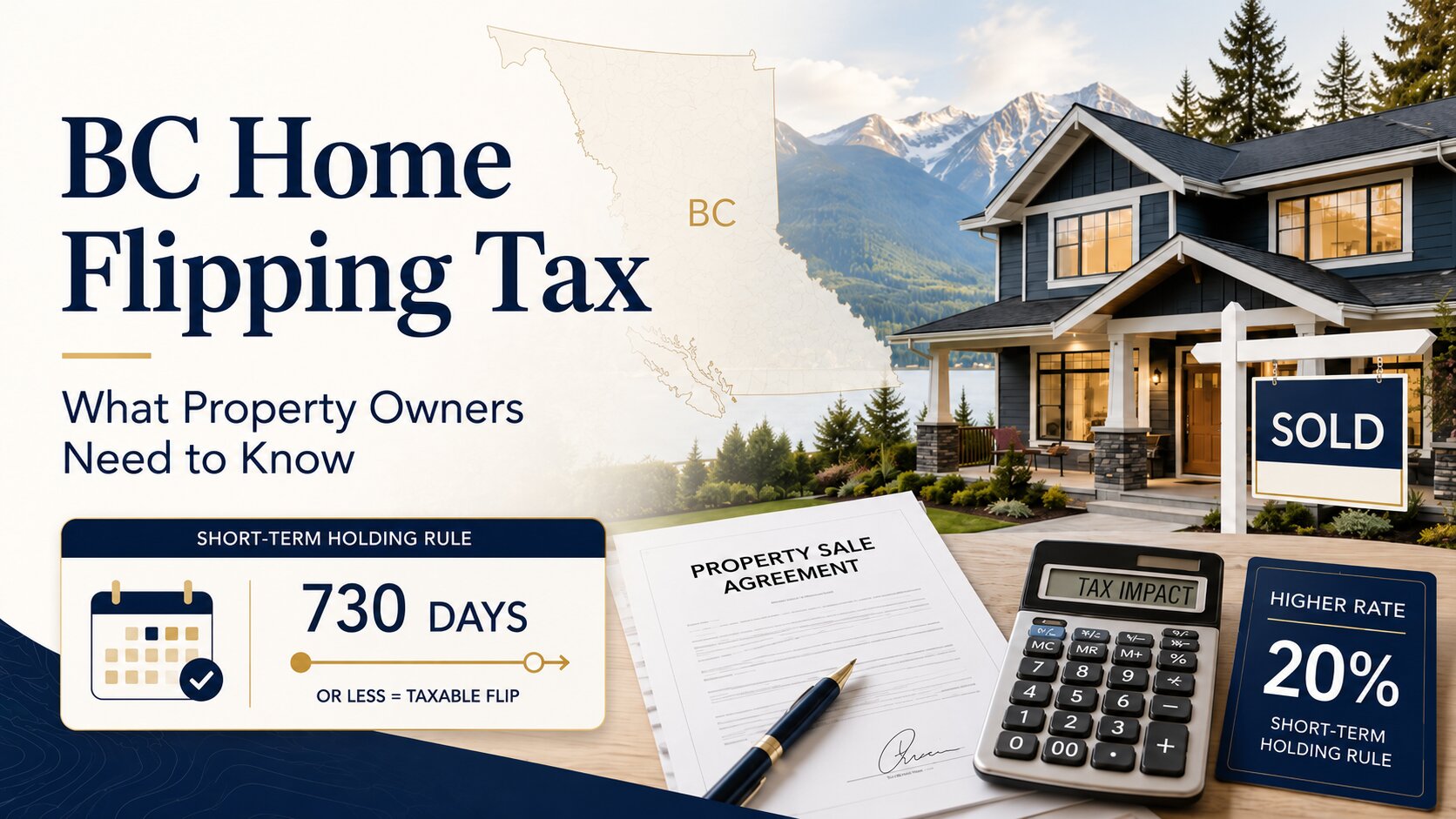

British Columbia’s home flipping tax took effect on January 1, 2025, and it applies to far more transactions than its name suggests. If you sell, transfer, assign, or reorganize ownership of residential property in BC within 730 days of acquiring it, the tax may apply, even if your sale has nothing to do with flipping.

The tax is formally called the Residential Property (Short-Term Holding) Profit Tax, and it is separate from both federal income tax and BC income tax. It has its own rules, its own filing requirements, and its own exemptions. Many property owners, and even experienced advisors, are surprised by how broadly the tax reaches.

This guide explains the current rules as of 2025, including the tax rates, what counts as taxable property, which exemptions exist, how to file, and what to watch for if you are planning a property transaction. For background on how this tax was originally proposed, see Sunny’s earlier post on the proposed home flipping tax rules.

TL;DR: The BC home flipping tax applies a 20% tax on profit when residential property is sold within 365 days of acquisition, decreasing to zero by day 730. Properties purchased before January 1, 2025 are still subject if sold within 730 days. Many exemptions exist for life circumstances like death, divorce, and job relocation, but most require filing a flipping tax return within 90 days of the sale. Get legal advice before selling residential property you have held for less than two years.

How the BC Home Flipping Tax Works

The tax applies when you dispose of taxable residential property in British Columbia within 730 days of acquiring it. The tax rate starts at 20% of your net taxable income from the sale if the property is sold within the first 365 days, then decreases proportionally over the second year until it reaches zero at day 730.

Net taxable income is calculated as the sale proceeds minus the cost of acquisition and the cost of improvements. This calculation is different from the capital gains calculation under the Income Tax Act, and the differences matter. For example, maintenance costs are not added to the cost of acquisition or improvement, so they do not reduce your net taxable income for this tax. Only costs that qualify as improvements to the property itself are deductible.

There is a primary residence deduction of up to $20,000 that can reduce the net taxable income if certain conditions are met. This deduction is specifically for properties that served as your primary residence.

The 730-Day Clock

The 730-day period includes both the acquisition date and the disposition date. The key dates are the date of acquisition and the date of disposition, which in a standard residential transaction means the completion dates of the purchase and the sale.

There are important nuances to how the clock starts and stops:

- Pre-sale contracts: If you bought a pre-sale contract, completed on the unit, and then sold it, the acquisition date is the date the pre-sale contract was signed, not the completion date. This means the 730-day clock starts much earlier than many buyers expect.

- Consideration received before closing: The disposition date can be the date the first installment of consideration is received or receivable, which may be earlier than the actual closing date. This is an important consideration when drafting the purchase and sale agreement.

- Transfers between related persons: The acquisition date may trace back through the chain of related ownership, even if a person in the chain is not related to another person in the chain.

Properties Purchased Before January 1, 2025

The tax is not grandfathered. Properties purchased before January 1, 2025 are still subject to the tax if they are sold on or after January 1, 2025 and were owned for less than 730 days. If you bought a property in mid-2024 and sell it in mid-2025, the tax applies unless an exemption is available.

What Counts as Taxable Property?

The tax applies to residential property in BC. Specifically, “taxable property” means a beneficial interest in residential property, or a right to acquire a beneficial interest in residential property. This includes:

- A property with a housing unit (a self-contained residential unit with cooking, sleeping, bathroom, and living area facilities)

- Land zoned for residential use, including vacant land zoned residential

- The right to acquire residential property, such as an assignment of a pre-sale contract

The tax does not apply to property used exclusively for commercial purposes. It also does not apply to property located on First Nations reserve lands, treaty lands, or other specified First Nations lands.

What Counts as a Sale?

The tax uses a broad definition of “disposition.” It includes not only standard sales but also certain transfers, assignments, and income-tax-deferred transactions. A disposition occurs when the first installment of consideration is received or receivable.

The following are specifically excluded from the definition of a sale:

- A deemed disposition under the Income Tax Act, such as when a property holder passes away

- A mortgage or lien against a property

- A lease

- A gift

- Other transactions where a change in legal title occurs but there is no change in beneficial ownership

This broad definition is one of the reasons the tax reaches transactions that have nothing to do with flipping. If you are transferring property as part of an estate plan, a corporate reorganization, or a partnership restructuring, the flipping tax rules may apply even though no money changes hands.

Tax Rates at a Glance

| Holding Period | Tax Rate |

| 0 to 365 days | 20% of net taxable income |

| 366 to 729 days | Proportional decrease from 20% to 0% |

| 730 days or more | 0% (tax does not apply) |

The rate decreases proportionally over the second year. For example, if you sell the property 548 days after acquisition (roughly halfway through the second year), the rate would be approximately 10% of net taxable income.

Exemptions from the BC Home Flipping Tax

There are two classes of exemptions: those that require you to file a flipping tax return, and those that do not. Most exemptions require filing, which means you must submit a return within 90 days of the sale even if no tax is owed.

Exemptions Requiring a Flipping Tax Return

These exemptions can eliminate or reduce the tax, but you must still file a return to claim them:

Life circumstance exemptions:

- Death of the property owner or a close family member

- Serious illness or disability

- Divorce, separation, or relationship breakdown

- Job loss or required relocation for employment

- Threats to personal safety

- Addition of household members (such as marriage, or a parent moving in)

- Birth or adoption of a child

- Bankruptcy, insolvency, or foreclosure

- Destruction of the housing unit

- Expropriation

- Disposing of a property acquired by winning a lottery

- A year-long delay in construction completion

Property-related exemptions:

- Building or developing new residential property

- Substantial renovations to an existing property

- Delays in construction exceeding one year

- Builders and developers selling in the ordinary course of business

Transfers between related persons:

- Sales between related persons connected by blood, marriage, common-law partnership, or adoption

- This exemption can be extended to friendships in certain circumstances

- Transfers to a related corporation or partnership may also qualify

Exemptions NOT Requiring a Flipping Tax Return

These exemptions always apply and do not require a filing:

- Property located in an exempt location (First Nations reserve lands, treaty lands, other specified First Nations Band lands)

- An exempt entity selling property (government bodies, First Nations bodies, non-profit institutions)

- Property used exclusively for commercial purposes

All exemptions are nuanced. Whether a specific situation fits within an exemption depends on the facts, and proper legal advice should be sought to confirm eligibility before relying on one.

Filing a Flipping Tax Return

The BC home flipping tax is separate from your annual income tax filings. It requires its own return, filed within 90 days of the sale, if either of the following applies:

- You sell property after January 1, 2025 and held it for 729 days or less (and no exemption that does not require a filing applies), or

- An exemption applies, but only after you file a return to claim it

If the property was held for 730 days or more, or an exemption that does not require a return is available, no flipping tax return needs to be filed.

Trustees of bare trusts must file if the beneficial owner would be required to file. This is an important detail for anyone holding property through a trust structure.

The Rollover Trap: When Income Tax Deferrals Do Not Protect You

One of the most important things to understand about the BC home flipping tax is that it operates independently of the Income Tax Act. Transactions that qualify for tax-deferred rollover treatment under federal income tax rules, such as transfers to a corporation, amalgamations, or certain estate planning transfers, do not get the same protection under the flipping tax rules.

In fact, the problem is worse than simply losing the deferral. When a rollover occurs without consideration, the cost of acquisition for flipping tax purposes will often be $0, because no actual consideration changed hands. This means the entire sale proceeds could be treated as net taxable income, resulting in a much larger tax bill than expected.

If you are planning any of the following, the flipping tax should be part of your planning:

- Corporate reorganizations

- Gifts or estate planning transfers

- Trust settlements or distributions

- Joint tenancy severances

- Pre-sale assignments

- Developer structuring

- Partnership restructurings

Partnerships and Joint Ventures

Partnerships create special challenges under the flipping tax rules. Each partner is generally taxed separately based on changes in their beneficial interest. However, uncertainty remains about when partnerships are considered “related” to corporations for the purposes of the related-person transfer exemption.

If you hold property through a partnership or joint venture, early structuring and legal advice are essential. The rules are technical and the consequences of getting it wrong are significant.

How the Flipping Tax Differs from Federal Property Flipping Rules

The federal government also has property flipping rules under the Income Tax Act. Under the federal rules, profits from selling a property held for less than 365 days are generally taxed as business income rather than capital gains, unless a qualifying exemption applies.

The BC home flipping tax is additional to the federal rules. You could face both the federal income tax treatment and the BC flipping tax on the same transaction. The two systems have different definitions, different exemptions, and different filing requirements. Qualifying for an exemption under one system does not automatically qualify you under the other.

Who Is Most at Risk?

The tax was designed to discourage short-term property speculation, but it reaches a much wider group of property owners. You should pay particular attention if you are:

- A homeowner who needs to sell within two years of buying due to life circumstances

- An investor who buys, renovates, and resells residential property

- A pre-sale buyer who plans to assign the contract before completion

- A property owner planning an estate transfer or corporate reorganization involving residential property

- A partner in a joint venture or partnership that holds residential property

- A trustee of a bare trust that holds residential property

For a broader look at the legal considerations of investing in BC real estate, see our guide on real estate investing in BC.

Frequently Asked Questions

How do I avoid the BC home flipping tax?

The most straightforward way to avoid the tax is to hold the property for 730 days or more before selling. If you must sell earlier, you may qualify for one of the life circumstance exemptions, such as death, divorce, serious illness, job relocation, or safety threats. These exemptions require filing a flipping tax return within 90 days of the sale. Each exemption has specific conditions, so get legal advice to confirm you qualify before relying on one.

Does the BC home flipping tax apply to my primary residence?

The tax can apply to a primary residence if it is sold within 730 days of acquisition. However, there is a primary residence deduction of up to $20,000 that can reduce the net taxable income. If you are selling your primary residence due to a life circumstance such as a job relocation or relationship breakdown, you may also qualify for a life circumstance exemption.

Does the tax apply to properties purchased before January 1, 2025?

Yes. The tax applies to any sale on or after January 1, 2025 where the property was held for less than 730 days, regardless of when it was purchased. If you bought a property in 2024 and sell it in 2025 within the 730-day window, the tax applies unless an exemption is available.

Do I need to file a flipping tax return if I qualify for an exemption?

In most cases, yes. The majority of exemptions, including all life circumstance exemptions, require you to file a flipping tax return within 90 days of the sale. Only a few exemptions do not require a filing: property on First Nations land, sales by exempt entities (government, First Nations, non-profits), and property used exclusively for commercial purposes.

What is the difference between the BC home flipping tax and the federal property flipping rules?

The federal rules, under the Income Tax Act, treat profits from selling a property held for less than 365 days as business income rather than capital gains, unless an exemption applies. The BC home flipping tax is a separate provincial tax that applies to residential property sold within 730 days. The two systems have different definitions, different rates, and different exemptions. You could be subject to both on the same transaction.

Does the tax apply to pre-sale assignments?

Yes. If you assign a pre-sale contract, the acquisition date for flipping tax purposes is the date you signed the pre-sale contract, not the completion date. This means the 730-day clock starts earlier than many buyers expect, and the tax may apply even if you assign the contract before the unit is completed.

What happens if I transfer residential property to a family member?

Transfers between related persons may qualify for an exemption. Related persons include those connected by blood, marriage, common-law partnership, or adoption, and the exemption can be extended to friendships in certain circumstances. However, the acquisition date may trace back through the chain of related ownership, which affects the 730-day calculation. This exemption requires filing a flipping tax return.

Get Legal Advice Before You Sell

The BC home flipping tax is highly technical and can apply to transactions that have nothing to do with flipping. If you are planning to sell, transfer, gift, or reorganize ownership of residential property in British Columbia that you have held for less than two years, professional advice is essential, especially when trusts, partnerships, corporations, or pre-sales are involved.

Sunny Tathgar is a real estate lawyer in Victoria BC who helps property owners understand and plan for the BC home flipping tax. Contact Tathgar Law for a free consultation.