Starting a business in British Columbia involves more than choosing a name. One of the first decisions is how the business should be structured. For many business owners, the options can feel confusing at first. Some people start on their own as sole proprietors. Others go into business with a partner. Some choose to incorporate right away, while others wait until the business grows.

Each structure has different legal and practical effects. It can affect personal liability, taxes, ownership, contracts, record keeping, and how the business can grow over time.

This article explains the main types of business structures in BC, including sole proprietorships, partnerships, and corporations. It also explains where business name registration fits into the process.

Quick Comparison: BC Business Structures

Each business structure serves a different purpose. The right choice depends on ownership, risk, growth plans, and how much structure the business needs.

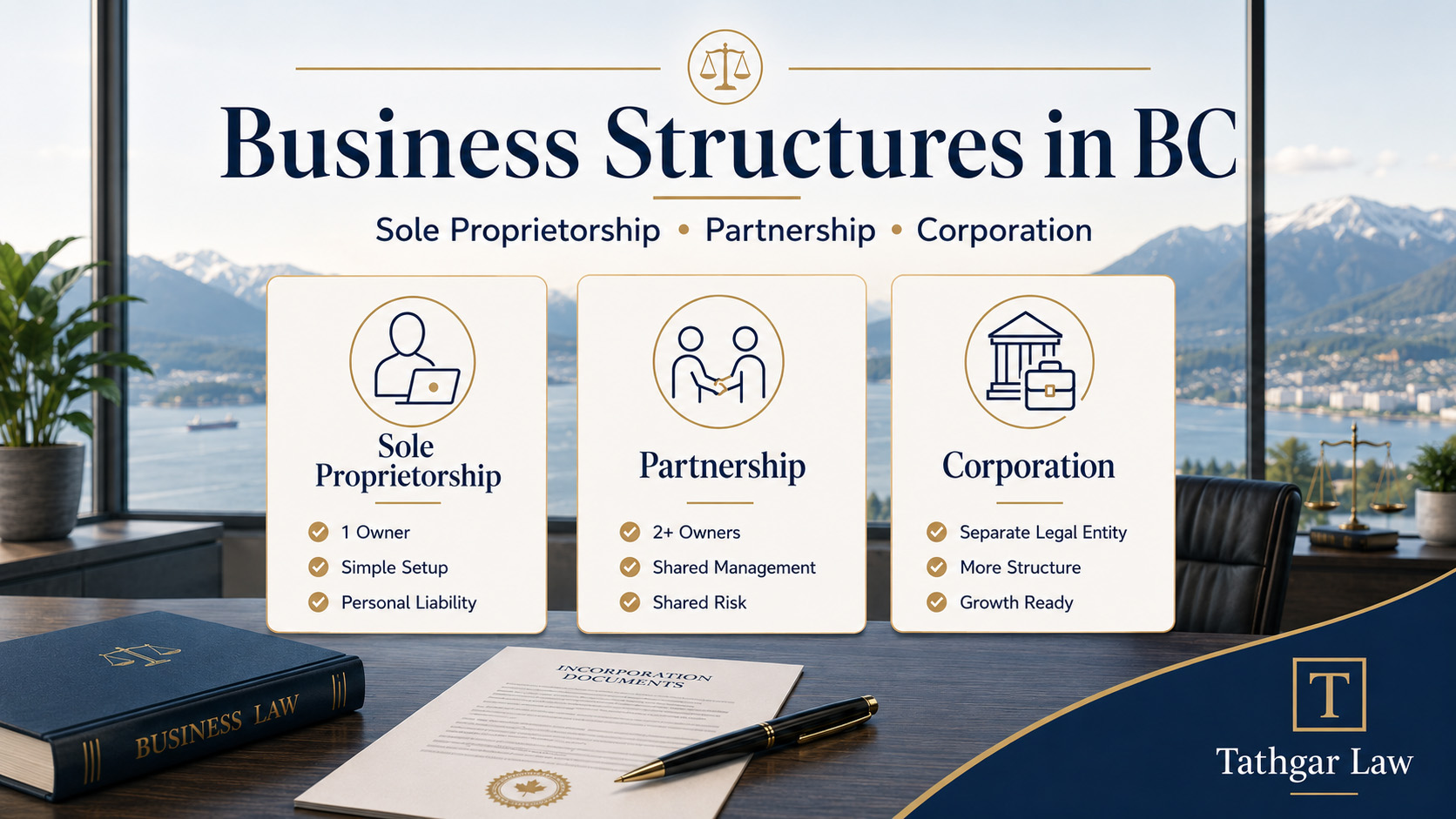

| Business Structure | Often Best For | Key Benefit | Main Concern |

| Sole Proprietorship | One person starting a simple business | Simple to set up and manage | The owner may be personally responsible for business debts and claims |

| Partnership | Two or more people running a business together | Allows shared ownership and shared decision-making | Partners may be personally responsible for business obligations, and disputes can arise without a written agreement |

| Corporation | Businesses with more risk, growth plans, employees, contracts, or multiple owners | Creates a separate legal entity with a clearer ownership structure | Requires more records, filings, and ongoing maintenance |

What Is a Sole Proprietorship?

A sole proprietorship is a business owned and operated by one person. It is often the simplest way to start a business in BC.

Many freelancers, consultants, tradespeople, and small service providers begin as sole proprietors because the setup is usually straightforward. The owner may operate under their own legal name or under a registered business name.

For example, a person named Sarah Lee may operate as “Sarah Lee.” If she wants to operate as “Island Admin Services,” that business name may need to be reserved and registered.

A sole proprietorship does not create a separate legal entity. The owner and the business are legally connected. This means the owner may be personally responsible for business debts, lawsuits, lease obligations, unpaid invoices, and other liabilities.

When a Sole Proprietorship May Make Sense

A sole proprietorship may be suitable when one person owns the business, the business is small or new, setup costs need to stay low, the business has lower liability risk, and the owner wants direct control.

This structure can also work when a person is testing a business idea before deciding whether to incorporate. The main concern is personal liability. If the business takes on debt or faces a claim, the owner’s personal assets may be exposed.

What Is a General Partnership?

A general partnership is a business owned by two or more people. Like a sole proprietorship, a general partnership is not separate from the owners in the same way a corporation is.

Partnerships can be useful when two or more people want to operate a business together. Each partner may contribute money, labour, knowledge, contacts, equipment, or other resources.

A partnership can also create legal risk. In many cases, partners may be personally responsible for business debts and obligations. One partner’s actions may also create risk for the other partners.

For that reason, a written partnership agreement is often a practical step before money changes hands, contracts are signed, or clients are served.

What Should a Partnership Agreement Cover?

A partnership agreement can set out ownership percentages, each partner’s role, contributions of money or labour, profit sharing, decision-making, banking authority, debt responsibility, dispute resolution, exit rights, and what happens if a partner dies or becomes unable to work.

Without clear written terms, business disagreements can become harder and more expensive to resolve.

What Is a Corporation?

A corporation is a separate legal entity. This means the corporation exists apart from its shareholders, directors, and officers.

A corporation can own property, enter contracts, borrow money, hire employees, sue, and be sued in its own name. The owners hold shares in the corporation rather than owning the business assets directly.

Incorporation is often considered when a business has liability risk, multiple owners, employees, contractors, commercial contracts, outside investors, or plans for growth.

When Incorporation May Make Sense

A corporation may be suitable when the business has more legal or financial risk, has more than one owner, plans to hire employees, is entering larger contracts, may bring in investors, may be sold later, or needs a clearer ownership structure.

Incorporation can help separate personal and business liability, but it does not remove every type of personal risk. Directors may still have legal duties. Owners may also create personal risk by signing personal guarantees, failing to remit taxes, or mixing personal and corporate finances.

Business owners should also speak with an accountant before incorporating because the tax effects depend on income, expenses, family circumstances, and long-term plans.

Where Does Business Name Registration Fit In?

Business name registration is part of the setup process for many businesses, but it is not the same as choosing a legal structure.

A business owner may need to reserve and register a name when operating a sole proprietorship or partnership under a name that is not only a personal legal name.

A corporation may also need name approval if it is being incorporated under a chosen name. Some corporations use a numbered company instead, such as “1234567 B.C. Ltd.” A numbered company can operate legally, though many businesses choose a named corporation for branding reasons.

In other words, name registration can apply to different structures. The bigger legal question is not just what the business should be called, but how the business should be legally structured.

Questions to Ask Before Choosing a Business Structure

Before choosing a business structure, it helps to look at how the business is expected to operate.

A sole proprietorship may be enough for a simple one-person business with lower risk. A partnership may make sense when two or more people are building the business together. A corporation may be worth considering when there are larger contracts, employees, financing needs, liability concerns, or plans to sell the business in the future.

Business owners should think about:

- Who will own the business?

- Will there be more than one owner?

- How much legal or financial risk does the business carry?

- Will the business sign a lease or larger contracts?

- Will the business hire employees or contractors?

- Will the business need financing?

- Could the business be sold later?

- What happens if one owner wants to leave?

- What happens if an owner becomes unable to continue working?

These questions can help narrow the options and show when legal or accounting advice may be needed before moving forward.

Can a Business Change Structure Later?

Yes. Many businesses start as sole proprietorships and incorporate later. This can make sense when a business is new, small, or still being tested.

As the business grows, incorporation may become more suitable. A business may reach a point where it has more income, more liability risk, employees, partners, financing needs, or long-term plans that call for a corporate structure.

Changing structure later can involve legal, accounting, tax, banking, and contract steps. Business owners may need to transfer assets, update agreements, open new bank accounts, revise tax accounts, and notify clients or suppliers.

Why Legal Advice Matters

Choosing a business structure is more than an administrative step. It affects how the business is owned, who is responsible for debts, how decisions are made, and what documents may be needed.

A lawyer can help with:

- Choosing a business structure

- Incorporating a company

- Preparing corporate records

- Drafting shareholder agreements

- Reviewing partnership agreements

- Reviewing contracts and commercial leases

- Supporting business purchases and sales

An accountant should also be involved where tax planning is part of the decision.

Related business law reading:

• Incorporating a Business in British Columbia: The Pros and Cons

• How to Incorporate a Business in Canada: A Step-By-Step Guide

• Shareholder Agreements in BC: Why They’re Essential

Sunny Tathgar assists business owners with incorporation, shareholder agreements, corporate records, business purchases, and other business law matters in BC.

FAQs

What are the main types of business structures in BC?

The most common business structures in BC are sole proprietorships, general partnerships, and corporations. Each structure has different legal, tax, ownership, and liability considerations.

Is business name registration the same as incorporation?

No. Business name registration is part of setting up or naming a business. Incorporation creates a corporation, which is a separate legal entity.

Does a sole proprietorship need to register a business name in BC?

A sole proprietor may need to register a business name if operating under a name other than their own legal name. A business owner should confirm the current requirements before starting.

Is a corporation always better than a sole proprietorship?

No. A corporation may offer more structure and liability separation, but it also comes with more records, filings, and costs. A sole proprietorship may be enough for a small, lower-risk business.

Do business partners need a written agreement?

Yes, a written agreement is often recommended. A partnership agreement can help prevent disputes by setting out ownership, duties, profit sharing, exits, and decision-making rules.

Can a sole proprietorship become a corporation later?

Yes. Many BC businesses start as sole proprietorships and incorporate later. The transition may require legal, accounting, banking, and contract updates.

Speak With Sunny Tathgar About Business Structures in BC

The right business structure can support a business from the start and reduce legal problems later. Whether starting a new business, adding a partner, incorporating a company, or reviewing corporate records, legal advice can help clarify the next step.

Contact Sunny Tathgar today to discuss business structures, incorporation, shareholder agreements, or other business law needs in BC.